You may have heard in your econ class about a good’s elasticity of demand, or about “elastic” or “inelastic” goods. Consumers’ elasticity of demand is just a fancy way economists talk about how sensitive people are to changes in a good’s price.

Take pizza for example. If suddenly all pizza costs two times what it normally does, how much pizza would you buy? Because of the Law of Demand - which says that as the price of a good increases, the quantity demanded decreases - we know that as the price of pizza goes up, you’ll buy less pizza, whereas if the price of pizza goes down (or was free!) you’d probably buy (or take) more. If the price of pizza doubled, you’d almost certainly buy less of it.

Elasticities of demand are a way to understand how much people change the quantity they demand in response to a change in prices. If the price of pizza doubled, would you and your friends only buy two pizzas instead of three? Or, would you only buy one slice each instead? Or, maybe you wouldn’t buy pizza at all and you’d get chicken wings instead. In all cases, the price increase of pizza causes you to buy less of it, but in each case the total decrease changes, from three pizzas down to two, one slice each, or zero slices. This example demonstrates different consumer sensitivities - or elasticities of demand - for pizza.

Elasticity of demand is usually denoted as an epsilon with a D subscript:

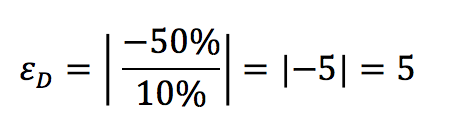

Mathematically, it is calculated by dividing the percentage change of a quantity of a good purchased by the percentage change in that good’s price, and then taking the absolute value:

Because of the absolute value function, the elasticity of demand will always be positive, with higher values indicating that consumers are more elastic, meaning they are more sensitive to price changes and reduce their quantity demanded more if the good’s price increases. (One way to think of this is like a rubber band - a very “elastic” rubber band will stretch a lot when you pull on it, while an “inelastic” rubber band will be harder to stretch.)

Imagine that, instead of doubling, the price of pizza rises by only 10%. If your demand for pizza is very elastic, and you drastically reduced the quantity of pizza you bought by 50% in response to this price increase, then we would know that your elasticity of demand for pizza is:

Generally, if a good has an elasticity of demand greater than 1 the good is said to have an elastic demand, and if the good has an elasticity of demand less than 1, then the good is said to have an inelastic demand.

Importantly, elasticity of demand is not the slope of the demand curve! This is a common mistake, and would be a perfect trick question on an economics exam. The slope of a demand curve affects a good’s elasticity, but they are not the same thing.

What are some things that might affect a good’s elasticity of demand?

- The number of available substitutes: For example, there are typically a lot of pizza chains located in cities, so if one brand tries to raise its prices, it is easy for its customers to switch to a different brand. If there is only one pizza shop in your area, it will be able to raise prices and only lose relatively few customers since those who demand pizza lack alternatives. Higher numbers of available substitutes for a good makes the elasticity of demand higher for that good.

- Share of income spent on the good: In general, people pay attention to the things they spend the most money on. If the price of gum doubles, you might not even notice. But if the price of your housing doubles, you’re definitely going to notice, and will be more likely to change your demand for housing (e.g. by moving to a cheaper place) in response. (Remember, elasticities are calculated with percentage changes, so these are actually comparable cases!) The bigger the share of a person’s income is spent on a good, the more elastic the demand for that good tends to be.

- Long vs. short run: In the short run, people have less time to alter their choices in response to price changes. If the price of gasoline doubles tomorrow, and people need gas to get to work, they will still buy and use the same amount of gasoline the next day, which might make it seem as if they have an inelastic demand for gasoline. But ,if gasoline prices stay high in the long run, people may decide to stop driving to work and instead take public transportation or carpool, both of which reduce the quantity of gasoline they use. In the long run, demand is more elastic than in the short run.

Important Elasticities (and how to draw them.

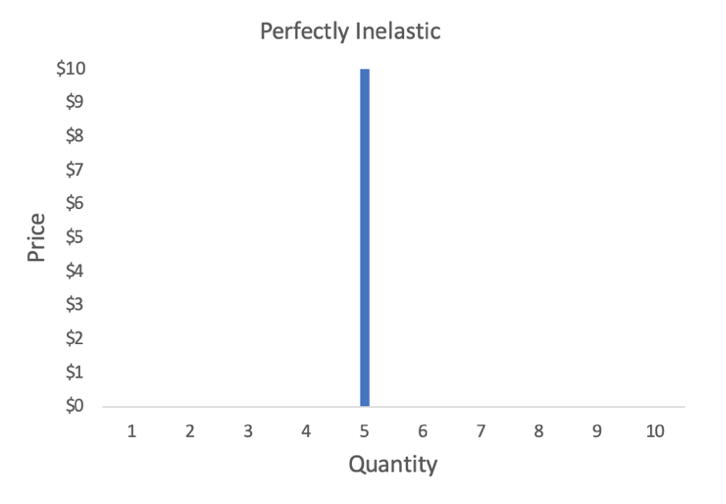

- Perfectly Inelastic: If the elasticity of demand is zero:

In this case, as the price changes people do not change the quantity that they buy. It means that the demand for the good doesn’t change as the price changes. In reality, probably no goods are perfectly inelastic, but many goods are very inelastic. Research in economics shows that services like healthcare or goods like cigarettes are examples of products that are very (though not perfectly!) inelastic.

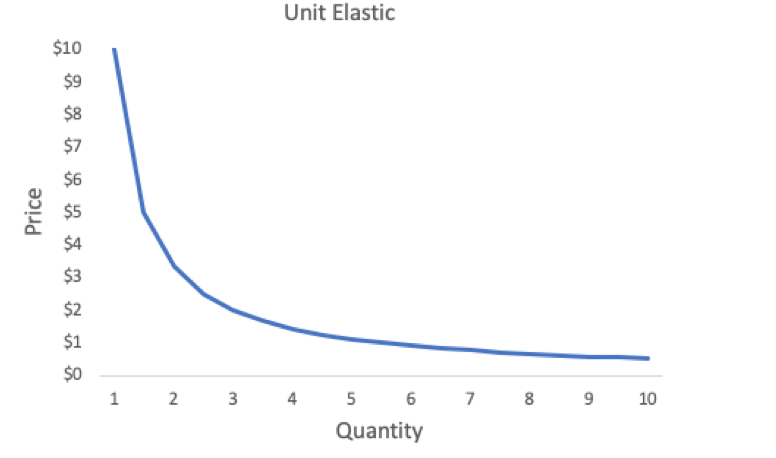

- Unit Elastic: If the elasticity of demand is one:

In this case, at any point on the curve, a percent change in price will cause an exactly equal percent change in quantity. So, if the price of a unit elastic good increases by exactly 10%, then the quantity demanded of the good will decrease by exactly 10%. This is true at any point on the graph. Notice again that this is not the slope of the demand curve.

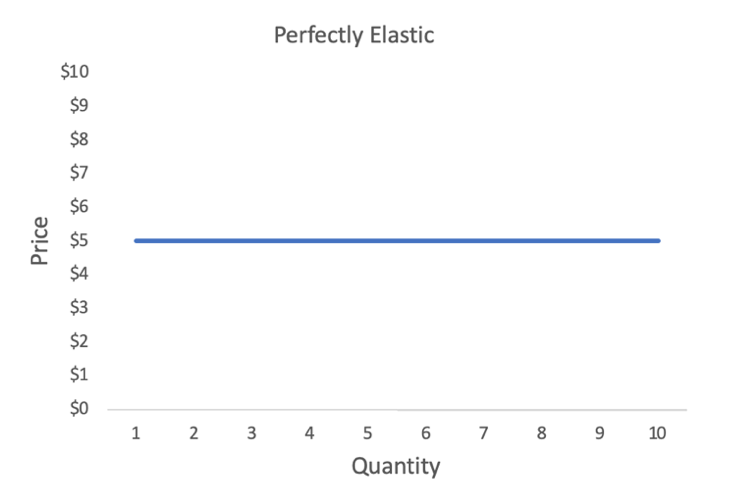

- Perfectly Elastic: If the elasticity of demand is infinity:

In this case, even the smallest increase in price will cause consumers to reduce their quantity to zero. Again, in reality there are probably no perfectly elastic goods, but there are many that are very elastic where people are very sensitive to price changes. Some goods, like brands of clothing, or activities, like eating out at a particular restaurant, are considered to have relatively high elasticities.

The figures above also can help you remember that goods with steep demand curves (more vertical) are more inelastic, while those with flatter demand curves are more elastic.

Comments